The Economic Outlook and Options for Fiscal Policy

Editor's Note: We generally don't think of government officials prognosticating on the record regarding future economic policy. As a former journalist in Washington, D. C., I'm used to the labyrinth that you sometimes have to overcome in order to get the information you need. For example, press officials at the U.S. Department of Commerce and the Office of Management and Budget were polite but direct: “We don't forecast.” Indeed, we generally look to them for after-the-fact statistics.

However, checking with the Congressional Budget Office turned up a gem. Not only did I find a recent forecast (fourth quarter, 2010), Douglas W. Elmendorf, director of the budget office, was the official who presented the information. Ironically, his audience was the Forecasters Club of New York, people who must divine the economic future as a part of their profession. This presentation is an invaluable sneak peek into the thought processes driving the current administration's fiscal policy. While your instinct may be to disagree, focus more on how these various fiscal policies could impact your business in 2011.

Here is what Elmendorf shared with his audience.

Congressional Budget Office Presentation to the Forecasters Club

The Economic Outlook and Options for Fiscal Policy

October 27, 2010

Douglas W. Elmendorf, Director

Introduction

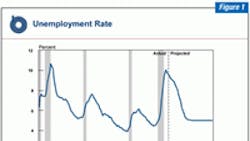

CBO expects that the economic recovery will proceed at a modest pace, leaving the unemployment rate above 8 percent until 2012. There are monetary and fiscal policy options that, if applied at a sufficient scale, would increase output and employment during the next few years (but not overnight). Such options would have costs as well. Expansionary fiscal policy would increase federal debt, which is currently larger relative to the size of the economy than it has been in more than 50 years — and is headed higher. (See Figures 1-4.)

Monetary Policy Options

The traditional tool of lowering the federal funds rate is not available. Based on comments of FOMC participants, the most important available tool appears to be the ability to buy additional longer-term securities.

-

Uncertainties: How much will a given amount of purchases reduce interest rates? How much will a decline in interest rates spur spending?

-

Risks: Can the Federal Reserve withdraw the additional stimulus quickly later? Should the Federal Reserve become more involved in capital markets?

Fiscal Policy Options

Options include changing many different types of federal spending and taxes. Two key questions:

-

What sorts of fiscal policies would encourage greater economic activity and more employment?

-

How can short-term fiscal stimulus be reconciled with the imperative to put fiscal policy on a sustainable medium-term and long-term path?

CBO has done a substantial amount of analysis on both of those questions.

What Sorts of Fiscal Policies Would Encourage More aEconomic Activity?

Policies can work through several channels, such as changing:

-

Demand for goods and services directly;

-

Current and/or expected income;

-

The payoff from extra work and saving;

-

The cost of investment.

Many policies work through more than one channel.

Predicting the effects of particular policies is difficult, and estimates are quite uncertain.

The American Recovery and Reinvestment Act (ARRA)

In CBO's assessment, ARRA has boosted output and employment relative to what would have occurred otherwise. The alternative cannot be observed, so any assessment must be inferred indirectly. Some concerns have been expressed about CBO's approach — but we believe we have accounted for them or they have little impact under current circumstances:

-

People saved, rather than spent, some of the tax cuts.

-

Jobs are shifting to different sectors and regions.

-

Interest rates might have been pushed up.

-

Other economic activity was crowded out.

CBO's Analysis of Some Specific Fiscal Options

CBO addressed policy options in a January 2010 report, “Policies for Increasing Economic Growth and Employment in 2010 and 2011.” We studied temporary policy changes. We estimated the “bang for the buck” of different policies; the effect on the economy would also depend on the scale of the policies. Making a significant difference in an economy with output of nearly $15 trillion would involve a considerable budgetary cost. We analyzed illustrative policies and provided ranges of estimates to reflect uncertainty. We focused on the short-term effects of the policies. (See Figure 5.)

How Can Fiscal Stimulus be Reconciled with Putting Fiscal Policy on a Sustainable Path?

There is no intrinsic contradiction between providing additional fiscal stimulus today, while the unemployment rate is high and many factories and offices are underused, and imposing fiscal restraint several years from now, when output and employment will probably be close to their potential. If taxes were cut permanently or spending increased permanently, that would worsen the fiscal outlook. Achieving both stimulus and sustainability would require a combination of policies: changes in taxes and spending that widen the deficit now, but reduce it relative to current projections after a few years.

CBO's Analysis of Extending the Expiring Tax Cuts

Extend the 2001 and 2003 tax cuts; extend higher exemption amounts for the AMT; reinstate the 2009 estate tax (adjusted for inflation). CBO presented the results in testimony to the Senate Budget Committee last month. The methodology was quite similar to the methodology we follow in analyzing the President's budget each spring. We used several different models and made a range of different assumptions about people's behavior. (See Figures 6-9.)

If Policymakers Want to Combine a Near-Term Boost with Medium-and Long-Term Restraint

If policies were enacted that widen the deficit in the near term, observers might question whether, when and how the difficult actions to narrow the deficit later would be carried out. To overcome their skepticism, those later actions would probably need to be specified and enacted into law. The enactment of policies that improved the budget outlook beyond the next few years would help to reduce uncertainty about government policies.

Conclusion

The economic recovery will probably proceed at a modest pace — leaving total output well below its sustainable level, and the unemployment rate well above its sustainable level, for a number of years. There are monetary and fiscal policy tools that would improve economic conditions during the next few years — though with costs and risks in the medium and long term. To avoid worsening the fiscal outlook, any policies that widen budget deficits in the near term would need to be accompanied by specific policies to reduce spending or increase revenue over time.