The Construction Industry: Focus on Forecasting

The construction industry is a notoriously cyclical sector of the economy. However, the direction of the cyclicality is relatively predictable. It is this predictability that is key in providing both wholesalers and building contractors with guideposts in managing their businesses. Below we outline the major factors driving the construction markets and their lead-lag relationship with the overall economic cycle.

The basis to understanding the over-all construction markets is the bifurcation between the residential construction and nonresidential construction markets. These two markets have differing cycles that can dampen or accentuate the overall construction cycle and demand for HVAC equipment. Typically, residential construction is considered an early cycle industry that leads the economy. In a classic economic cycle, residential construction moves upward for two to three years before cycling downward as interest rates rise. Just as rates rise, nonresidential construction begins its journey upward, not peaking until two years after the overall economic cycle turns down, at which point residential construction is already beginning its upward move. Thus, the two cycles offset each other, leading to small cyclical moves in the overall construction cycle. Unfortunately, reality is much messier than the classic cycle would indicate. These cycles often do not line up neatly to offset each other. Instead, they often accentuate the ups and downs of the overall construction industry. We shall discuss each cycle in turn, their timing, and the likely interplay between the two cycles this time.

The residential construction cycle, in reality, can be either early cycle or mid cycle. The key determinant in these two outcomes is the shape of the previous cycle. In normal real estate cycles, as occurred in the 1960s and 1970s, residential construction was an early cycle industry. Even in the early 1980s, it exhibited its typical early cycle characteristics. However, the 1980s saw an extended economic cycle that prolonged the housing upturn through 1987 and witnessed prices moving out of line with underlying consumer incomes. The decade then ended in a financial crisis, requiring the government to rescue the financial system. Preceding this crisis, the housing cycle began a multiyear descent from its 1987 peak, not bottoming until 1993, two years after the recapitalization of the financial system. The residential construction market then began a gradual multiyear rise, not peaking until the late 1990s. However, prices and physical construction remained within normal bounds, and there were no problems in the financial system. Thus, once the economy started to bottom and interest rates fell, as the Federal Reserve cut rates to stimulate the economy, housing exhibited its early cycle characteristics.

Page 2 of 2

The residential construction cycle was set to turn downward once more in 2004, when the Federal Reserve and presidential administration encouraged banks to provide mortgages without the normal 20 percent down payment. This move to create incremental demand by relaxing lending standards extended the housing cycle and ultimately led to the housing bubble in 2005 - 2006. Once the bubble burst and housing prices turned downward, the relaxed lending standards came back to haunt the banks, as the mortgages proved uncollectible. This led to a financial crisis similar to that of the early 1990s, which required another recapitalization of the banking system. Based on the normal six year peak-to-trough time period in such circumstances, the residential construction market should begin its upturn in late 2011. In fact, if we were to examine the market today, residential construction is actually running up on a year-over-year basis according to the latest statistics. With home builders reporting strong order growth for third quarter 2011, this upturn should accelerate as the economy moves into 2012.

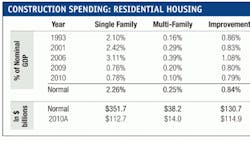

There are two other factors to consider when looking at the shape and strength of the residential construction cycle. They are the existing level of construction and demographics. First, demographics determine the number of housing units required to be constructed. Currently that number is 1.4 million to 1.5 million units per year, which is a combination of normalized household formation of 1.1 million to 1.2 million per annum coupled with the need to replace more than 300,000 units of the housing stock annually. Existing housing starts are 600,000 units, well below normalized demand. Second, construction spending for both single-family and multifamily units is running well below normalized levels as a percent of GDP. In 2010, single-family construction was only 0.8% of GDP while multifamily comprised 0.1 percent of GDP. The normalized levels for these are more than 2.25 percent+ and more than 0.25 percent respectively. Thus, once the cycle gains strength, one should expect overall housing starts to return to the 1.4 million to 1.5 million level by 2014-2015 or two and a half times the current level.

Nonresidential construction is typically a mid- to late-cycle industry, lagging the economic cycle by two years. The principal reason the lag is so long relates to employment and the time from initial commercial start until completion. Thus, as the economy turns down, buildings and projects under construction continue until completed. At the same time, government typically stimulates the economy by increasing expenditures on public works, such as road construction. This typically delays the downturn in commercial construction until economic recovery is underway. Thus, the nonresidential construction industry experiences its downturn as the economy exits a recession. In fact, nonresidential construction typically plummets as a percent of GDP during this time from its normal peak of 2.8 percent to 3.0 percent of GDP to just 1.7 percent to 1.9 percent of GDP, which is where the industry currently resides. Recovery is delayed for two reasons. First, projects are finished that add to capacity in the economy after capacity utilization has turned down during the recession, thus increasing excess capacity. Second, employment is a lagged function to economic growth. Thus, job growth and absorption of space do not occur until after the economy has been growing for some time. When coupled together, this typically means the economy must grow for two-plus years before nonresidential construction bottoms as occurred in the 1970s, 1980s, 1990s and 2000s.

Other factors must be considered going forward. With the rise of retailing over the Internet, the need to construct new malls should lessen over time, while the demand for modern warehouse and distribution space should rise. In fact, due to strong growth in their Internet sales, major retailers such as BestBuy plan to shrink their store footprints as leases come up for renewal. Thus, as the cycle turns upward, the mix of buildings to be constructed should change.

If we were to look at where both the residential and nonresidential construction cycles stand today, it appears that both are set to turn upward together. Thus, with overall construction standing at just 3.5 percent of GDP, it appears poised to grow strongly over the next few years, potentially reaching over 6 percent of GDP by 2015. Thus, as construction industry participants look ahead over the next few years, they should plan on growth to the upside in 2012 and beyond.

Paul Sloate is president and CEO of Green Drake Partners, an independent investment management firm, that focuses on assisting its clients with the preservation and growth of their wealth. Contact Paul at 610/687-7766, [email protected] or visit www.greendrakepartners.com.